There is a before and after in almost every financial journey — a moment when things were genuinely hard, and a moment when something shifted and everything started moving in a better direction.

For me, the shift did not come from a raise. It did not come from a windfall or an inheritance or a lucky break. It came from a collection of small, consistent habits that I built one at a time — habits so simple that they almost seem too straightforward to produce the results they actually delivered.

The budget habits that changed my life are not complicated. They do not require a finance degree, a spreadsheet obsession, or a personality transformation. They require consistency — showing up for your financial life every day with the same small intentional behaviors until those behaviors become automatic and the results become undeniable.

If you are in the before of your financial story and looking for the habits that will take you to the after — this is the honest account of what actually worked.

Contents

- 1 Why Budget Habits Matter More Than Budget Plans

- 2 Habit #1: Writing Down Every Dollar Before the Month Begins

- 3 Habit #2: Paying Myself First — Automatically

- 4 Habit #3: The Sunday Money Check-In

- 5 Habit #4: The 24-Hour Purchase Pause

- 6 Habit #5: Meal Planning Every Single Sunday

- 7 Habit #6: The Monthly Subscription Audit

- 8 Habit #7: Building a Cash Buffer — One Month Ahead

- 9 Habit #8: Tracking Net Worth Monthly

- 10 The Cumulative Impact of These 8 Habits

- 11 How to Build These Habits Without Overwhelm

- 12 Frequently Asked Questions

- 13 Q: Which budget habit should I start with first?

- 14 Q: How long does it take for budget habits to change your financial situation?

- 15 Q: What if I fail at a habit and have a bad spending week?

- 16 Q: Do I need special apps or tools to build these habits?

- 17 Q: Can these habits work on a very low income?

- 18 Conclusion

Why Budget Habits Matter More Than Budget Plans

Most people approach budgeting by making a plan. They sit down, create a detailed spreadsheet, assign money to every category, and feel genuinely motivated by the clarity and intentionality of what they have created.

Then life happens. An unexpected expense. A stressful week. A social event that requires spending. And the plan — which required willpower to maintain — collapses under the weight of real life.

The problem with budget plans is that they rely on conscious decision-making every single day. And conscious decision-making requires willpower — which is finite, unpredictable, and completely unreliable under stress.

Budget habits are different. A habit, by definition, is something you do automatically — without thinking, without deciding, without using willpower. Once a budget habit is established, it runs in the background of your life regardless of stress, busyness, or emotional state.

This is why the budget habits that changed my life have lasted — not because I am particularly disciplined or financially sophisticated, but because these behaviors became automatic long ago and now happen without any conscious effort at all.

Habit #1: Writing Down Every Dollar Before the Month Begins

This was the first budget habit that changed my life — and the one that made every other habit possible.

Before this habit, I operated on a vague sense of my finances. I knew approximately how much I earned and approximately how much I spent — and I trusted that approximate sense to keep me on track. It never did.

The zero-based budget — writing down every expected income and every planned expense before the month begins, until income minus expenses equals zero — replaced approximation with intention. Every dollar was assigned a job before it could be spent unconsciously.

How I built this habit:

On the last day of every month, I sit down for 30 minutes with a notebook or the EveryDollar app. I list every expected income source. Then I list every planned expense in priority order — necessities first, savings second, lifestyle spending third. Every dollar is assigned.

The first month felt uncomfortable and revealing. I discovered I had been spending $340 per month on restaurants, $180 on coffee shops, and $200 on online shopping — none of which felt like significant individual decisions but together represented $720 per month of money I had no clear accounting for.

The result: Within 60 days of this habit, I had more money at the end of the month than I could ever remember having — not because my income had changed but because my awareness had.

Annual impact: $3,000–$8,000 saved through intentional allocation.

Habit #2: Paying Myself First — Automatically

The second budget habit that changed my life is the one most people know about intellectually but very few actually implement correctly.

Paying yourself first means automating a savings transfer to happen the moment your paycheck arrives — before you pay bills, before you buy groceries, before you do anything else with the money.

Most people save what is left over at the end of the month. There is never anything left over.

How I built this habit:

I logged into my bank account and set up an automatic transfer for the day after my payday — $50 initially, because that felt manageable. The transfer moved money from my checking account into a high-yield savings account at Ally Bank before I ever saw it or could spend it.

Within three months, I increased to $100. Then $200. Then $300. Each increase happened after I adjusted to the previous amount without missing the money — which happened faster than I expected every single time.

The key insight is that you always spend what you have. When less money is available in your checking account, you naturally adjust your spending to that reduced amount without feeling deprived — because the money is not gone, it is simply somewhere you cannot see or easily access it.

Annual impact: $2,400–$6,000 saved automatically.

Habit #3: The Sunday Money Check-In

This is the budget habit that most surprised me with its impact — because it takes only 15 minutes once per week and yet consistently prevents the spending drift that undoes most budgets.

Every Sunday morning — same time, same day — I spend 15 minutes reviewing the past week’s spending against my monthly budget. I open my bank app and look at every transaction from the past seven days. I categorize each one. I see where I am against my budget in each category.

This is not a punishment exercise or a shame spiral. It is simply awareness maintenance — keeping the clear picture of my finances that I established at the beginning of the month from becoming blurry again.

What the Sunday check-in catches:

Subscription charges I forgot about. Restaurant spending that crept up without me noticing. A pattern of small purchases in one category that are collectively larger than I realized. The occasional purchase that I regret and that serves as useful information about my spending triggers.

The critical function: The Sunday check-in gives me the information I need to adjust the remaining weeks of the month before the situation is unrecoverable. If I have overspent on groceries by day seven — I know by day eight and can course-correct for the remaining three weeks. Without the check-in, I would not know until the end of the month when there is nothing left to do about it.

Annual impact: Prevents $1,000–$3,000 in monthly budget overruns.

Habit #4: The 24-Hour Purchase Pause

The fourth budget habit that changed my life eliminated more unconscious spending than any other single behavior change — and it requires almost no willpower because it simply inserts time between the impulse and the action.

How the habit works:

Any time I feel the urge to buy something non-essential, I add it to a list on my phone — the item and the price. I do not act on the urge immediately. I wait 24 hours minimum, 48 hours ideally.

When I return to the list the next day, one of three things has happened. I have forgotten about the item entirely — meaning the urge was momentary and not a genuine want. The desire has faded significantly — meaning it was emotional rather than rational. Or I still genuinely want it and it fits my budget — in which case I buy it without guilt.

What I discovered: Approximately 80 percent of my impulse purchase urges disappear completely within 24 hours. The items I add to the list that I still want 48 hours later are almost always purchases I am genuinely glad I made. The habit separates genuine desires from reflexive spending.

Annual impact: $2,000–$5,000 in impulse purchases avoided.

Habit #5: Meal Planning Every Single Sunday

Meal planning appears on almost every budget habit list — because it consistently delivers the highest financial return of any single frugal behavior for most American families.

Before this habit, I was spending $150 to $200 per week on groceries plus $100 to $150 per week on restaurants and delivery — over $1,300 per month on food alone.

The meal planning habit reduced this to $60 to $80 per week on groceries and virtually zero on restaurants and delivery — a reduction of $800 to $900 per month from one habit change.

How the habit works:

Every Sunday, I spend 20 minutes planning seven dinners for the coming week. I check what I already have in the refrigerator, freezer, and pantry first — building meals around existing ingredients reduces both cost and waste. I write a specific grocery list from the meal plan. I buy only what is on the list.

The meal plan removes the daily decision of what to have for dinner — which is the decision that leads to delivery orders when you are tired, hungry, and have nothing ready to eat. When dinner is already planned and the ingredients are already home, delivery is never tempting because the problem it would solve does not exist.

Annual impact: $8,000–$12,000 saved on food spending.

Habit #6: The Monthly Subscription Audit

Subscriptions are the budget leak most people do not notice until they add them all up — and then the total is consistently shocking.

The budget habit of auditing subscriptions on the first day of every month takes 15 minutes and reliably uncovers money leaving my account for services I forgot I signed up for, services I tried once and never returned to, and services that have gradually stopped providing value worth their monthly cost.

My audit process:

Open my bank statement. Search for recurring charges. List every subscription with its monthly cost. Ask one question about each: did I use this at least once this month and did it provide value worth the cost? Anything with a no answer — canceled immediately.

What this habit has revealed over time:

A fitness app I used for two weeks and forgot about for eight months — $15/month for $120 in value received. A news site subscription that I visited twice — $10/month. A software subscription that I had upgraded and then the upgrade became unnecessary — $8/month. A streaming service I was paying for that my family had collectively stopped using — $16/month.

These individual amounts feel small. Combined and compounded over time they represent hundreds of dollars per year leaving silently for things that provide essentially zero value.

Annual impact: $300–$1,500 recovered from forgotten subscriptions.

Habit #7: Building a Cash Buffer — One Month Ahead

This is the budget habit that delivers the most dramatic emotional result — the feeling of genuine financial peace rather than constant financial anxiety — even before the numbers change dramatically.

Operating one month ahead financially means that the money I earn in June pays for my July expenses. My June bills are paid with money I earned in May. There is always one month of expenses sitting in my checking account as a buffer against the unexpected.

This sounds impossible when you are living paycheck to paycheck. It is not — it just takes time to build.

How I built this habit:

I started by saving $500 — just enough to create a tiny buffer against the most common unexpected expenses. Then I rebuilt my monthly budget slightly tighter and directed the difference toward the buffer until it reached one full month of expenses.

The process took approximately four months. The emotional transformation was immediate and dramatic. The constant low-level anxiety of “what if something goes wrong before payday” disappeared the moment the buffer existed. That anxiety had been so present for so long that I had normalized it — and its absence felt remarkable.

Annual impact: Not measurable in dollars — measured in financial peace, better sleep, and the ability to make financial decisions from a position of stability rather than desperation.

Habit #8: Tracking Net Worth Monthly

The final budget habit that changed my life is the one that makes every other habit feel meaningful and worth maintaining long-term.

Net worth — the total of everything you own minus the total of everything you owe — is the most honest single number representing your financial health. And tracking it monthly transforms abstract financial habits into visible, concrete progress.

How I track it:

On the first of every month, I spend 10 minutes calculating my net worth. I list every asset — savings account balance, checking account balance, retirement account balance, any property value. I list every liability — credit card balances, student loans, car loans, mortgage. Assets minus liabilities equals net worth.

I record this number in a simple note on my phone — just the date and the number.

The first month I tracked, my net worth was negative — more debt than assets. Seeing that number was uncomfortable. But seeing it improve month after month — $200 better, then $500 better, then $1,000 better — as the budget habits accumulated and compounded was one of the most motivating experiences of my financial life.

The psychological power: Every budget habit feels abstract until you can see its impact in a number that changes every month. The net worth tracker makes the abstract concrete — and the concrete motivating.

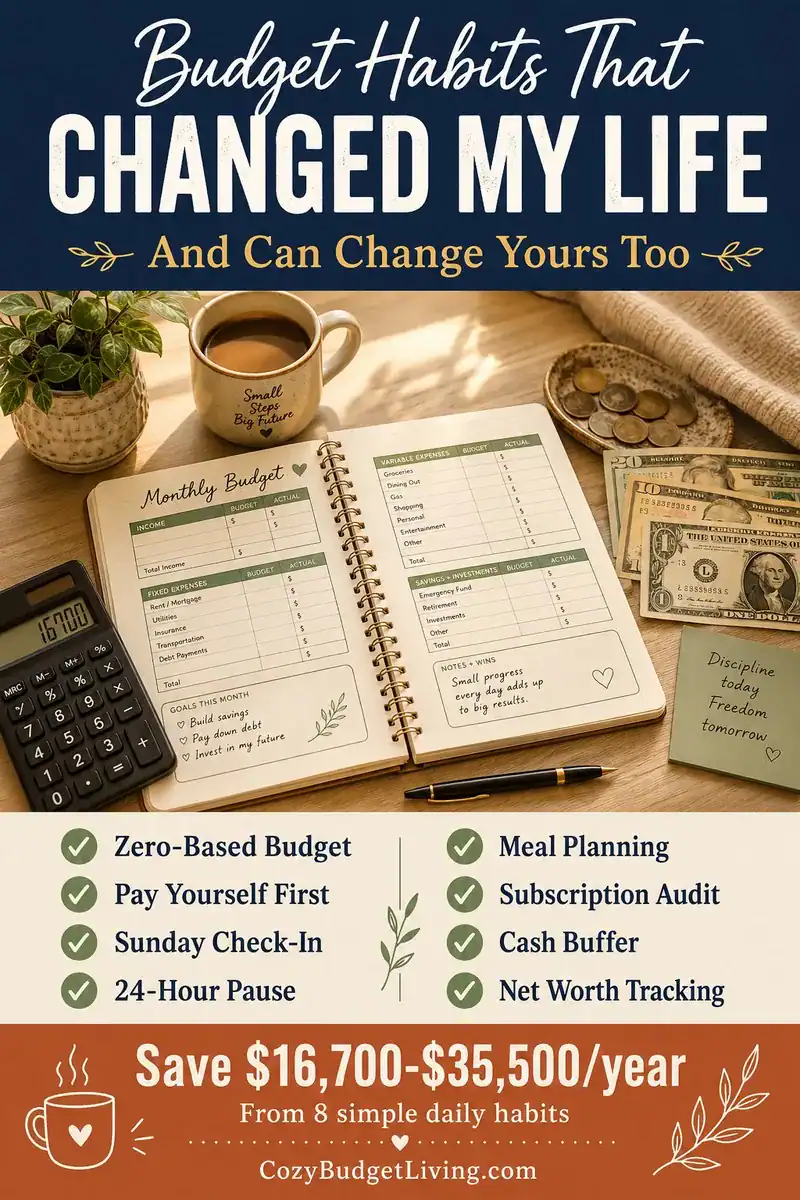

The Cumulative Impact of These 8 Habits

| Habit | Annual Financial Impact |

|---|---|

| Zero-based monthly budget | $3,000–$8,000 saved |

| Pay yourself first | $2,400–$6,000 saved |

| Sunday money check-in | $1,000–$3,000 in overruns prevented |

| 24-hour purchase pause | $2,000–$5,000 in impulse avoided |

| Weekly meal planning | $8,000–$12,000 saved |

| Monthly subscription audit | $300–$1,500 recovered |

| One-month cash buffer | Financial peace (priceless) |

| Monthly net worth tracking | Compounding motivation |

| Total measurable impact | $16,700–$35,500/year |

How to Build These Habits Without Overwhelm

The biggest mistake people make when reading a list like this is trying to implement all eight habits simultaneously. This approach almost always fails — too much change at once creates overwhelm that leads to abandoning everything.

The approach that actually works:

Pick one habit. Just one. The one that resonates most strongly with your current situation or feels most immediately manageable. Practice it every day for 30 days until it requires almost no conscious effort.

Then add the second habit. Practice both for 30 days.

Continue until all eight habits are running automatically in the background of your financial life — which takes approximately eight months if you add one habit per month.

Eight months of gradual habit building versus eight months of white-knuckling a rigid plan that eventually collapses. The habit approach wins every time — not because it is more dramatic but because it lasts.

Frequently Asked Questions

Q: Which budget habit should I start with first?

The zero-based monthly budget and the pay-yourself-first automatic savings transfer are consistently the highest-impact starting points. The monthly budget creates awareness. The automatic savings creates momentum. Together they produce results within 30 to 60 days that motivate everything that follows.

Q: How long does it take for budget habits to change your financial situation?

Most people notice meaningful improvement within 60 to 90 days of consistently practicing three to four of these habits. Dramatic financial transformation — paying off significant debt, building substantial savings, reaching real financial peace — typically takes 12 to 24 months of consistent habit practice.

Q: What if I fail at a habit and have a bad spending week?

Continue. A bad week does not erase the progress of the previous weeks or months. Financial habits are built over years — one imperfect week is insignificant in that timeline. What matters is returning to the habit as quickly as possible rather than using one failure as permission to abandon the entire system.

Q: Do I need special apps or tools to build these habits?

No — a notebook and a bank statement are sufficient for every habit on this list. That said, apps like EveryDollar (budget), Ally Bank (high-yield savings), and Empower (net worth tracking) make each habit significantly easier to maintain consistently. All have free versions sufficient for these purposes.

Q: Can these habits work on a very low income?

Yes — with modified expectations about the pace of progress. The habits themselves are income-independent. Pay yourself first works at any income level — even $10 per paycheck builds the habit and creates momentum. The Sunday check-in and subscription audit recover money at any income level. Meal planning saves proportionally regardless of income. Start where you are with what you have.

Conclusion

The budget habits that changed my life did not change it by being dramatic. They changed it by being consistent — small, repeatable behaviors that accumulated quietly into results I could not have predicted when I started.

Zero-based budgeting gave me clarity. Automatic savings gave me momentum. The Sunday check-in gave me awareness. The purchase pause gave me intentionality. Meal planning gave me hundreds of dollars back every month. The subscription audit recovered money I did not know I was losing. The cash buffer gave me peace. Net worth tracking gave me proof that it was all working.

Pick one habit from this list today. Just one. Practice it for 30 days. See what happens.

Your financial after is closer than you think — and it starts with one habit, practiced today.

Save this post to Pinterest and come back to it every month as you build each new habit! 📌

Related Posts You’ll Love: